LAWSUITS

N CASE LAW

LAWSUITS

-

RE: PAY TO PLAY

Concerning Count 52, several witnesses testified that Pawlowski obtained lists of vendors who had City contracts and described how Pawlowski used these lists to solicit campaign contributions and determine how much in contributions each vendor should give.

-

RE: LIEN ASSIGNMENTS

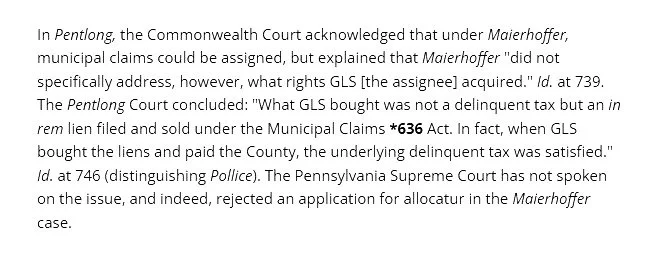

In Pentlong, the Commonwealth Court acknowledged that under Maierhoffer, municipal claims could be assigned, but explained that Maierhoffer "did not specifically address, however, what rights GLS [the assignee] acquired." Id. at 739. The Pentlong Court concluded: "What GLS bought was not a delinquent tax but an in rem lien filed and sold under the Municipal Claims *636 Act. In fact, when GLS bought the liens and paid the County, the underlying delinquent tax was satisfied." Id. at 746 (distinguishing Pollice). The Pennsylvania Supreme Court has not spoken on the issue, and indeed, rejected an application for allocatur in the Maierhoffer case.

-

RE: 2 laws of collection

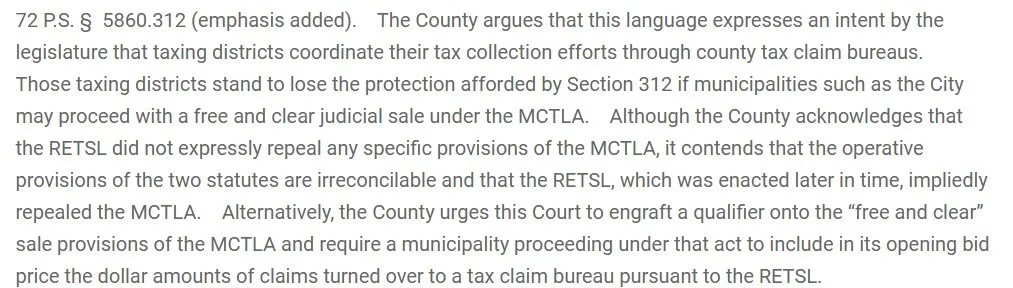

To permit the City of Allentown to proceed with judicial sales of two properties pursuant to the Municipal Claims and Tax Liens Act (MCTLA). At issue is whether the properties can be sold “free and clear” of liens for taxes levied by the County, or whether divestiture of such liens is precluded by the Real Estate Tax Sale Law (RETSL).

-

RE: WRIT OF MANDABUS

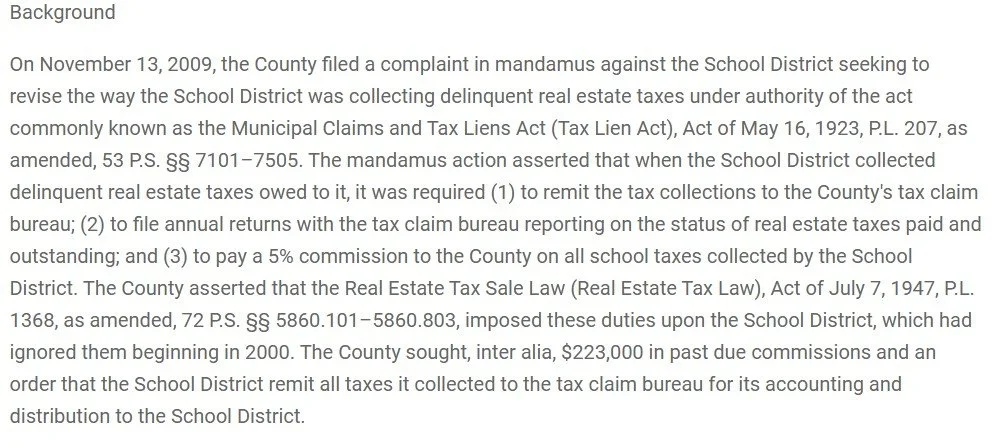

Disposes of the County's claim for retroactive commissions or its demand that all tax payments collected by the School District must be made payable to the tax claim bureau.

-

RE: Delegation of TAX COLLECTION TO A FOR-PROFIT AGENCY

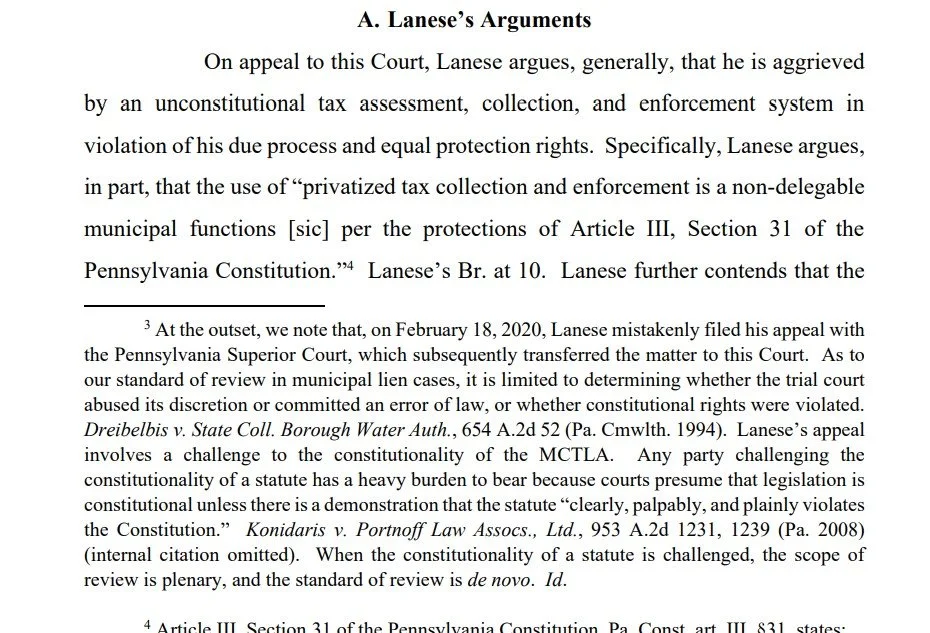

Based on the information provided, Lanese's argument that "privatized tax collection and enforcement is a non-delegable municipal function per the protections of Article III, Section 31 of the Pennsylvania Constitution" is centered on the principle that the power to levy taxes and perform municipal functions generally cannot be delegated to private entities.

Article III, Section 31 of the Pennsylvania Constitution, titled "Delegation of certain powers prohibited", states that: "The General Assembly shall not delegate to any special commission, private corporation or association, any power to make, supervise or interfere with any municipal improvement, money, property or effects, whether held in trust or otherwise, or to levy taxes or perform any municipal function whatever".

Lanese contends that the use of privatized tax collection and enforcement falls under this constitutional prohibition against delegating core municipal functions, including the power to levy taxes.

Essentially, Lanese's argument challenges the legality of using private companies to handle functions like tax assessment, collection, and enforcement, asserting that these are essential governmental responsibilities that cannot be outsourced under the Pennsylvania Constitution

-

RE: Where a legislative body acts in a governmental, as opposed to a proprietary, capacity, it cannot take any action which binds its successors

.A school district's determination as to whether a school should or should not be constructed is governmental in nature as its source is derived from Pennsylvania law.27.Specifically, 24 P.S. § 7-701 authorizes a school board to provide "suitable school buildings to accommodate all children."

328.Where a legislative body acts in a governmental, as opposed to a proprietary, capacity, it cannot take any action which binds its successors.Therefore, the School Board which entered into the Joint Development Agreement and/or Memorandum of Agreement could not bind the School Board which passed the December 6, 1995 Resolution to its determination that an elementary school would be constructed in Clifton Township. The trial court granted the preliminary objections on other grounds in an Order dated May 19, 1997, and dismissed Lobolito’s complaint with prejudice.

\\\Carbon hoping court hearing will help it reclaim delinquent taxes

Published December 10. 2010 05:00PM

BY AMY MILLER AMILLER@TNONLINE.COM

Carbon County officials are hoping their upcoming court hearing will help them reclaim delinquent taxes that were lost because Panther Valley School District utilized a third party tax collection agency instead of the county tax claim bureau.

During the county commissioners' meeting on Thursday, the board voted unanimously to add an addendum to a letter of understanding between the county and Riley and Company of Mount Pocono, from Aug. 21, 2009.The action is for additional services to assist in assessing the overall accuracy of Portnoff Law Associates' information on delinquent tax collections. The revised total compensation will be $85,000.The board also voted unanimously to have Infocon Corporation modify the current software to allow for the importing of unpaid tax claims to the tax claim bureau's current delinquent tax file and to comply with the Pennsylvania Real Estate Tax Sale Law requirements. The estimated cost will be $5,000.Commissioner William O'Gurek, chairman, explained the actions are in preparation for the county's hearing against the Panther Valley School District for using Portnoff, of Norristown, to collect delinquent taxes instead of the county tax claim bureau. The hearing is set for Dec. 21 in front of Judge Steven Serfass.The county is being represented by attorney Jane Maughan of Stroudsburg, the attorney who won a similar case in Monroe County, where the Commonwealth court ruled that delinquent tax collections need to go through the county tax claim bureau.Panther Valley is being represented by Sweet, Stevens, Katz, and Williams LLP of Pittston, which they hired in December 2009.O'Gurek explained that the county has a claim against a total of six taxing bodies Panther Valley, Weatherly, Jim Thorpe, and Hazleton school districts and the borough of Summit Hill for the practice of instructing tax collectors to turn over delinquent taxes to Portnoff instead of the county. All entities except Panther Valley School District ceased operation with Portnoff after the county notified them that there was a major issue, that is why the county filed a suit against Panther Valley last year."By turning over the delinquents to Portnoff, those taxing bodies destroyed the public records of taxes in Carbon County," he said. "The county code and state law says that the county's tax claim bureau is responsible to maintain these records."O'Gurek said that Riley, who has been under contract with the county since August 2009, has reviewed 364,000 transactions from the taxing bodies that have turned over records to date."We have a nightmare to say the least on taxing delinquents," he said, "In order to prepare for court and prepare our claims that we will use in the future against the other taxing bodies, we needed the monies (and Riley's audit) that were involved."The $90,000 that the county will spend to prepare the audit and update the Infocon system will also be part of the suit, O'Gurek said, adding that the county will seek to have that added expense paid by the school districts as "part of the costs associated with righting the wrong that had been done.""It's a sad state of affairs but these taxing bodies turned over delinquent taxes to a law firm down the turnpike and took the records out of Carbon County that the law says should be in Carbon County," O'Gurek said. "There is $90,000 worth of costs associated with what they did, not to mention the monies that didn't come into the county because of what they did."Carbon County is entitled to 5 percent commission on all delinquent taxes collected, according to state law, but the county has not seen the money from the taxes because they were not collected through the county tax bureau.O'Gurek said, "That's part of the whole process because we now know how much was paid in on an annual basis. We're aware now of those monies the taxing bodies owe to the county, and that will be part of the case as well."Commissioner Charles Getz noted the county is owed hundreds of thousands of dollars in compensation from the six entities because of the 5 percent commission.O'Gurek said he feels the taxpayers are being held hostage because of the action by the taxing bodies and by the fees that Portnoff adds when collecting the delinquent taxes."The most unfair thing these taxing bodies did to the people who can ill afford to pay their taxes was turn it over to a vulture that slapped on an exorbitant fee and now it costs them a lot more money on what they cannot afford to pay to begin with," he said.In addition to the fees, Portnoff convinced those taxing bodies that they should put liens on the delinquents' properties, which has only created more problems.Commissioner Wayne Nothstein said that the elected officials are not the ones to blame in this situation because they were misled by Portnoff.Getz agreed, adding that he feels the blame lies in the solicitors of these boards, because they allowed them to hire Portnoff.O'Gurek said that the county will fight for the people and will pursue this matter until everything is resolved."They broke the law, resulting in no unified public records archive and we want to get it corrected," he said.The county has been working to obtain the thousands of delinquent tax records since early 2009.After discussions with Panther Valley failed to produce an agreement, the county filed suit against them in November 2009.The court action against Panther Valley seeks to have delinquent tax records that were collected by Portnoff, the firm hired by the school district to pursue the collection of delinquent real estate taxes from 2000 to the present, returned to the county, so that the Carbon County Tax Claim Bureau can have complete records of all property liens and delinquencies.It also seeks to obtain the 5 percent commission for each delinquent tax collection that the tax claim bureau is entitled to under the Pennsylvania Real Estate Tax Sale Law. According to the suit, that commission owed is at least $323,000 or more.Panther Valley used Portnoff because the company promised to get the delinquent tax money faster than the county, and its services would be of no charge to the district. The added expense for their services would instead be added to the delinquent taxpayer's bill.